Facing the daunting prospect of student loan default? Understanding the potential consequences is crucial for borrowers struggling to manage their student loan repayments. This article explores the serious ramifications of failing to meet your student loan obligations, detailing the impact on your credit score, financial stability, and future opportunities. We will examine the various stages of student loan delinquency, from initial missed payments to the ultimate repercussions of default, providing clear guidance on available options and resources to help you navigate this challenging situation. Learn how to avoid the devastating effects of student loan default and protect your financial future.

Student loan debt is a significant burden for many, and the inability to repay can have far-reaching and potentially devastating consequences. This guide will illuminate the complexities of student loan forgiveness programs, explore income-driven repayment plans, and discuss the potential for wage garnishment, tax refund offset, and other actions taken by lenders. We’ll provide a comprehensive overview of the legal processes involved, helping you understand your rights and options while offering practical strategies to address student loan debt and avoid the pitfalls of default. Don’t let student loan default derail your future – equip yourself with knowledge and regain control of your financial situation.

Grace Periods and What They Mean

A grace period is a temporary period after you finish your studies or leave your educational program, during which you are not required to make payments on your student loans. The length of this period varies depending on your loan type and lender, but it’s designed to provide a buffer for graduates as they transition into the workforce and begin their repayment journey.

Understanding Grace Periods: It’s crucial to understand that a grace period isn’t an extension of the loan itself; it’s simply a delay in the commencement of repayment. Interest may still accrue on your loans during this period, depending on your loan type. For example, subsidized federal student loans typically don’t accrue interest during the grace period, while unsubsidized loans do.

Types of Grace Periods: The duration and terms of your grace period will be clearly outlined in your loan documents. There are several types of grace periods, depending on the lender and loan program; some are short, perhaps only a few months, while others may extend to several years. You should always carefully review the terms of your loan agreement to understand the specific grace period associated with your student loans.

Impact on Your Credit Score: While you aren’t required to make payments during your grace period, it’s important to remember that failure to begin repayment after the grace period ends can negatively impact your credit score. Missed or late payments are reported to credit bureaus and can significantly lower your credit rating, making it harder to obtain credit in the future. It is crucial to understand the length of your grace period and plan accordingly to avoid negative consequences.

Contacting Your Lender: If you anticipate difficulties in repaying your student loans after your grace period ends, proactively contacting your lender is vital. They may offer various repayment options, such as income-driven repayment plans, deferment, or forbearance, to help you manage your debt more effectively.

Default vs. Delinquency Explained

Understanding the difference between loan delinquency and loan default is crucial for borrowers facing repayment challenges. While both indicate problems with repayment, they represent distinct stages in the process and carry different consequences.

Delinquency occurs when a borrower misses one or more scheduled student loan payments. The exact definition of delinquency varies depending on the lender, but generally, a payment is considered delinquent after it’s 30 days past due. During the delinquency period, the lender may charge late fees and report the missed payment to credit bureaus, negatively impacting the borrower’s credit score. However, the loan is still considered active, and there are usually opportunities to reinstate the payments and avoid further repercussions.

Default, on the other hand, is a far more serious situation. It typically occurs after a prolonged period of delinquency, usually after 9 months of missed payments (though this timeframe can vary by lender and loan type). Once a loan enters default, the consequences become much more severe. The lender may pursue aggressive collection tactics, including wage garnishment, tax refund offset, and even legal action. Furthermore, defaulting on student loans has a devastating impact on a borrower’s credit score, making it difficult to obtain credit in the future. It also may affect employment opportunities and other financial benefits.

The key distinction lies in the severity and permanence of the consequences. Delinquency is a warning sign, offering a chance for remediation. Default, however, signifies a complete breakdown in the repayment agreement, resulting in significant and long-lasting financial damage.

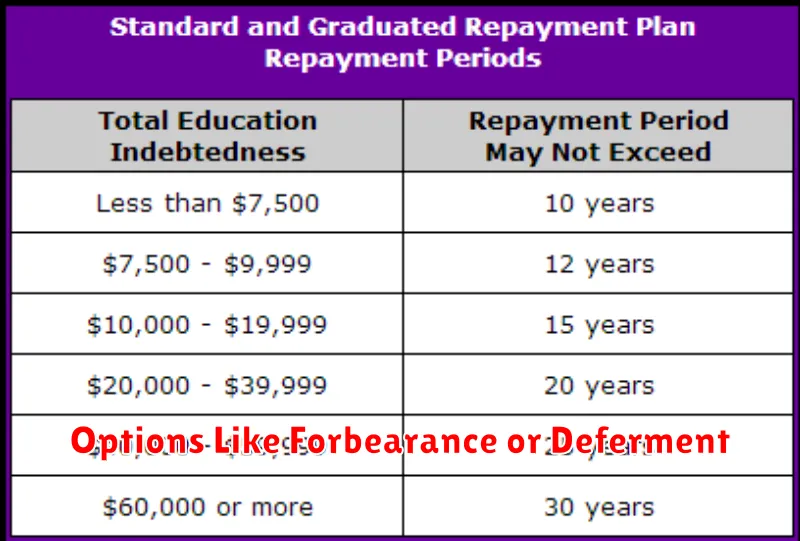

Options Like Forbearance or Deferment

If you find yourself unable to make your student loan payments, exploring options like forbearance or deferment may provide temporary relief. These programs temporarily postpone your payments, offering a much-needed break during financial hardship. However, it’s crucial to understand the nuances of each and their potential long-term implications.

Forbearance allows you to temporarily suspend or reduce your student loan payments for a specified period. Interest typically continues to accrue during forbearance, potentially leading to a larger balance upon resumption of payments. The length of forbearance can vary depending on your lender and circumstances. Various types of forbearance exist, each with its own criteria and stipulations. It is essential to discuss the details with your loan servicer to determine the most suitable forbearance option for your situation.

Deferment, similar to forbearance, postpones your loan payments. However, the key difference lies in the interest accrual. Depending on the type of loan and the reason for deferment, interest may or may not accrue during this period. This could result in significant long-term savings, unlike forbearance. Eligibility for deferment is often tied to specific circumstances, such as unemployment or enrollment in school. Understanding the eligibility requirements and the terms of your specific deferment plan is crucial.

Both forbearance and deferment offer short-term solutions. They are not designed as long-term fixes for repayment struggles. It’s important to develop a long-term repayment strategy to address the underlying financial challenges. Failing to do so could result in your loans entering default, triggering severe consequences.

Before opting for either forbearance or deferment, carefully consider the potential consequences, including the accumulation of interest and the impact on your credit score. Contact your loan servicer to discuss your options and explore the best path for your financial situation. They can provide personalized guidance and explain the specifics of each program.

Long-Term Credit Impact of Missed Payments

Missing student loan payments can have a profoundly negative long-term impact on your credit score. Even a single missed payment is recorded on your credit report and can significantly lower your creditworthiness.

The severity of the impact depends on several factors, including the number of missed payments, the amount owed, and the type of loan. Multiple missed payments will severely damage your credit, making it difficult to secure future loans, rent an apartment, or even get a job in some fields.

Your credit score, a crucial factor in financial decisions, will plummet. Lenders use this score to assess your risk as a borrower. A lower score means higher interest rates on future loans, limiting your access to credit and potentially costing you thousands of dollars over time.

Beyond the immediate credit score drop, missed payments can lead to loan default. This occurs when you haven’t made payments for a prolonged period, typically 90 days or more. Defaulting on a student loan has severe consequences, including wage garnishment, tax refund offset, and difficulty obtaining government benefits. Your credit report will reflect the default for up to seven years, making it extremely challenging to rebuild your credit.

Furthermore, missed payments can trigger collection agencies to pursue you for the outstanding debt. These agencies can aggressively pursue payment, impacting your personal and professional life. They may contact your family and friends, potentially damaging your relationships and reputation.

In short, the consequences of failing to repay your student loans extend far beyond the immediate financial burden. The negative impact on your credit history can hinder your ability to achieve various financial goals for years to come, highlighting the importance of proactive loan management and seeking help when facing repayment difficulties.

How to Contact and Negotiate With Loan Servicers

If you’re struggling to repay your student loans, contacting your loan servicer is crucial. They are the company responsible for collecting your payments and managing your account. Finding their contact information is usually straightforward; it’s typically listed on your monthly statement or on the servicer’s website. You can usually reach them via phone, mail, or through a secure online portal.

Once you’ve established contact, clearly explain your financial situation to your loan servicer. Be honest and provide documentation to support your claims, such as pay stubs or bank statements. This demonstrates your commitment to resolving the issue and increases the likelihood of a positive outcome. The more detail you provide about your financial hardship, the better equipped they are to help.

Negotiating with your loan servicer might involve exploring several options. Deferment postpones your payments for a specified period, while forbearance reduces or temporarily suspends your payments. Both options can provide temporary relief, but interest usually still accrues during these periods. Another possibility is an income-driven repayment plan, which bases your monthly payment on your income and family size. These plans can significantly lower your monthly payments, making them more manageable in the long term.

Remember to carefully review any agreement you reach with your loan servicer. Understand the terms and conditions fully before signing anything. It’s also wise to keep detailed records of all communication, including dates, times, and the outcomes of each conversation. This documentation protects you and ensures a transparent process. If you feel overwhelmed or unsure about the process, consider seeking professional guidance from a credit counselor or financial advisor.

Finally, be persistent and patient. Negotiating with loan servicers may require multiple attempts and conversations. Don’t be discouraged if your initial request isn’t immediately approved. Continue to proactively engage with your servicer and demonstrate your good faith efforts to repay your student loans.

Why Ignoring Loans Makes Things Worse

Ignoring your student loans might seem like the easiest option when facing financial hardship, but it will only exacerbate the problem. Failing to make payments doesn’t erase the debt; instead, it allows the principal balance to grow significantly.

Late fees and interest charges will accumulate rapidly, compounding the original debt. These additional costs can quickly inflate the total amount owed, making the loan even more difficult to repay in the future.

Furthermore, ignoring your loans can severely impact your credit score. Negative marks on your credit report stemming from missed or late payments will stay there for years, making it harder to secure loans, rent an apartment, or even get a job in the future. Many employers conduct credit checks as part of their hiring process.

Beyond the financial repercussions, ignoring your student loans can lead to legal consequences. Lenders can take legal action to recover the debt, potentially resulting in wage garnishment, bank levy, or even lawsuit. These actions can have a devastating impact on your personal and financial well-being.

Therefore, proactively addressing your student loan situation is crucial, even if it means seeking professional guidance. Contacting your lender to discuss repayment options is the first step toward finding a sustainable solution and mitigating the long-term damage of ignoring your obligations.

{kind=link}