Are you preparing to buy a home and feeling overwhelmed by the prospect of closing costs? Understanding what these costs truly encompass is crucial for budgeting and avoiding unpleasant surprises during the final stages of your mortgage process. This article will break down the often-confusing components of closing costs, offering a clear picture of what to expect and how to prepare for them. We’ll delve into the various fees involved, providing you with the knowledge to confidently navigate this significant financial step.

Beyond the initial down payment, closing costs represent a substantial expense that can significantly impact your overall budget. Many homebuyers underestimate the magnitude of these fees, leading to financial strain after the purchase. This guide will clarify the different types of closing costs, such as loan origination fees, title insurance, property taxes, and more. By understanding these costs, you can better negotiate with lenders, plan your finances effectively, and ultimately, achieve your dream of homeownership with peace of mind. We will also offer tips for minimizing your closing costs and avoiding hidden fees.

Understanding the Term ‘Closing Costs’

Closing costs are the various fees and expenses paid at the closing of a real estate transaction, typically a home purchase. These costs are separate from the down payment and the loan amount itself.

It’s crucial to understand that these costs are not optional; they are required to finalize the purchase. They cover a range of services and processes involved in transferring ownership of the property.

While the exact amount varies depending on location, the type of loan, and the specifics of the transaction, understanding what constitutes these costs is essential for accurate budgeting and financial planning.

Thinking of closing costs as the administrative fees associated with legally transferring the property deed from the seller to the buyer is a helpful analogy. This includes numerous services such as appraisals, title searches, and insurance.

Many buyers are surprised by the sheer number of individual fees that collectively make up the closing costs. Accurate estimations are crucial to avoid unexpected expenses at the last minute. It is advisable to discuss closing costs thoroughly with your lender and real estate agent during the pre-purchase phase.

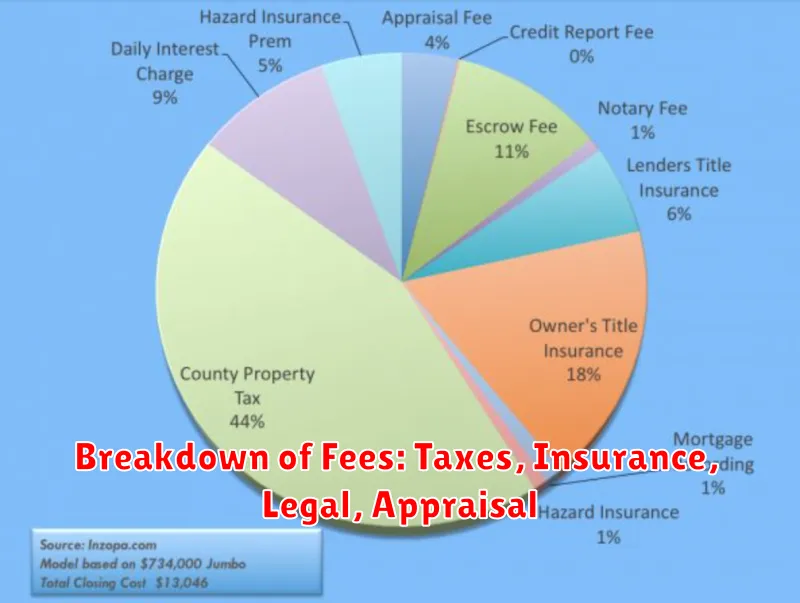

Breakdown of Fees: Taxes, Insurance, Legal, Appraisal

Property Taxes are levied annually by local governments and are typically paid in arrears. The amount due is usually pro-rated for the portion of the year the buyer owns the property. These funds support essential local services such as schools, roads, and public safety.

Homeowners Insurance is crucial to protect your investment. Lenders require proof of adequate coverage before closing to ensure the property is insured against damage or loss. Premiums are typically paid annually in advance, and the initial payment may be required at closing.

Legal Fees encompass the costs associated with legal representation during the closing process. While not always required, it’s advisable to have an attorney review the loan documents to protect your interests. Fees vary significantly depending on the lawyer’s hourly rate and complexity of the transaction.

Appraisal Fees cover the cost of a professional appraisal conducted to determine the market value of the property. Lenders require appraisals to ensure the property’s value justifies the loan amount. This ensures that they aren’t lending more money than the property is actually worth.

Understanding these key closing costs—property taxes, homeowners insurance, legal fees, and appraisal fees—is vital to budgeting effectively for your home purchase. Remember to inquire with your lender and closing agent for precise cost estimates specific to your situation, as amounts can vary based on location and property specifics.

How Much You Should Budget For

Estimating closing costs can feel daunting, but understanding the typical ranges helps you prepare financially. Closing costs typically range from 2% to 5% of the loan amount. This means that for a $300,000 home loan, you might expect to pay anywhere from $6,000 to $15,000 in closing costs.

However, this is just a broad estimate. The actual amount will vary based on several factors, including your location, the type of loan you obtain, and the specific services required in your transaction. Some areas have higher average closing costs than others. Similarly, a more complex loan or one with additional features may lead to higher fees.

To get a more accurate idea of what to expect, it’s crucial to review the Loan Estimate provided by your lender. This document, required by law, will detail all the anticipated closing costs. Pay close attention to the individual line items, noting any fees that seem unusually high. Don’t hesitate to ask your lender for clarification on any item you don’t understand.

Beyond the lender’s Loan Estimate, you should also factor in any additional expenses you might incur. These could include things like home inspections, appraisals, title insurance (which is often not fully included in the Loan Estimate), and pro-rated property taxes. It’s always wise to have a buffer built into your budget to account for unexpected costs that may arise during the closing process.

Finally, remember that you might need to pay for these closing costs out-of-pocket. While some lenders offer options to roll closing costs into your mortgage, this will increase your overall loan amount and increase the total interest you’ll pay over the life of the loan. Carefully weigh the benefits and drawbacks before making this decision.

How to Request an Estimate Early

Requesting an early estimate for your closing costs is a proactive step that can significantly benefit your home-buying process. It allows you to better understand the financial implications involved and budget accordingly, preventing any unpleasant surprises closer to the closing date.

Most lenders will provide a preliminary Loan Estimate relatively early in the process, often soon after your loan application is submitted and reviewed. This initial estimate outlines the projected closing costs, though it’s important to note that these figures may be subject to change. Factors like appraisal costs, title insurance, and recording fees can fluctuate.

To request this estimate, you should directly contact your lender. A simple phone call or email expressing your desire for a preliminary cost breakdown is usually sufficient. Be prepared to provide any necessary information they may request to expedite the process. Clearly stating your intention to understand potential closing costs early will ensure they prioritize your request.

While an early estimate offers a valuable overview, remember that it remains an approximation. Your final closing costs will be detailed on the official Closing Disclosure, which is provided at least three business days before closing. Nonetheless, an early estimate enables you to begin planning and saving for the expected expenses, reducing the financial stress associated with a large purchase.

By actively pursuing an early estimate, you demonstrate your financial responsibility and gain a crucial head start in managing the financial aspects of your home purchase. This proactive approach ensures you’re better prepared and informed throughout the entire process.

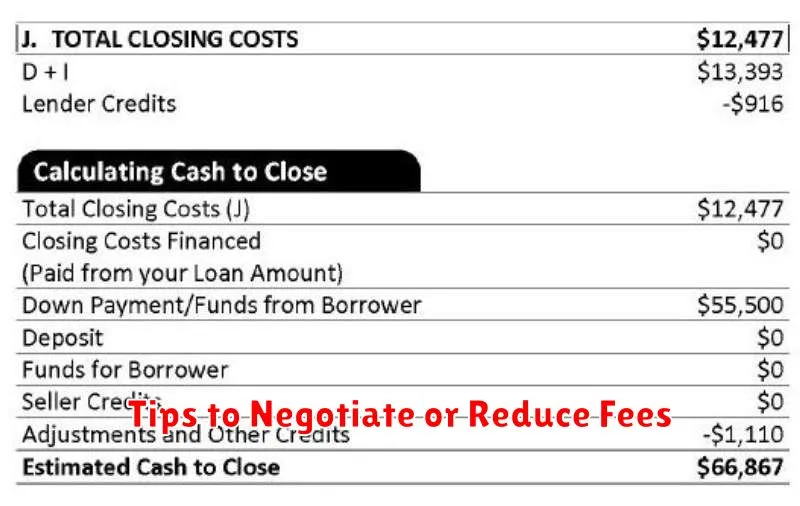

Tips to Negotiate or Reduce Fees

Negotiating closing costs can significantly impact your overall mortgage expenses. While some fees are non-negotiable, such as government recording fees and taxes, others are often open to discussion.

One effective strategy is to shop around for different lenders. Each lender may have varying fees and structures. Comparing quotes from multiple lenders allows you to identify those with the most competitive closing costs.

Furthermore, consider asking your lender for a detailed line-item breakdown of all fees. This transparency enables you to identify any potentially inflated or unnecessary charges. Questioning these items directly with the lender can sometimes lead to reductions.

Negotiating your interest rate can indirectly impact closing costs. A lower interest rate often leads to a lower upfront cost. This negotiation should be approached strategically, emphasizing your financial strength and creditworthiness.

Finally, inquire about the possibility of crediting fees toward your closing costs. Some lenders offer incentives, such as credits for using their preferred title insurance company, reducing your overall out-of-pocket expense. Be sure to carefully read all documentation and fully understand all terms and conditions before making any agreements.

Hidden Charges to Be Aware Of

While many closing costs are clearly outlined in the initial loan estimate, several potentially significant charges can sneak up on unsuspecting homebuyers. Understanding these hidden costs is crucial to budgeting effectively and avoiding unpleasant surprises at the closing table.

One often overlooked expense is the appraisal fee. While the lender may mention an appraisal, the actual cost is sometimes only revealed closer to closing. This fee covers the professional assessment of the property’s value, a necessary step in the mortgage process.

Homeowner’s insurance premiums are another area where hidden charges can emerge. The initial quote might not reflect all applicable taxes or fees, resulting in a higher-than-expected premium at closing. Carefully reviewing the final insurance policy is essential to avoid this pitfall.

Title insurance, while usually included in the initial estimate, can sometimes contain additional, unforeseen charges. Title insurance protects the lender and the homeowner from title defects, but the specific fees and add-ons can vary.

Pest inspections are not always explicitly mentioned upfront, but some lenders may require them. This additional cost can add several hundred dollars to your closing expenses, dependent on the size and scope of the home and the requirements of the lender.

Finally, recording fees, which are paid to the local government to officially record the mortgage, can also exceed initial estimates, especially in areas with higher local fees.

By being aware of these potentially hidden charges, homebuyers can better prepare financially for the closing process and avoid unexpected costs that can derail their home purchase.

{kind=link}