Improving your credit score is a crucial step towards achieving your financial goals, whether it’s buying a house, securing a loan with a favorable interest rate, or even renting an apartment. Many people mistakenly believe that improving their credit is a long and arduous process, but with a strategic approach to credit card use, you can significantly boost your score in a relatively short time. This article will guide you through practical and effective methods to leverage your credit cards to your advantage, focusing on smart usage strategies that will demonstrably improve your creditworthiness.

Understanding how your credit card habits impact your credit report is the first step towards positive change. This guide will delve into key factors like credit utilization, payment history, and the length of your credit history, demonstrating how responsible credit card management contributes to a higher credit score. We’ll explore strategies such as paying your bills on time, keeping your credit utilization ratio low, and diversifying your credit accounts to maximize the positive impact on your overall credit profile. Get ready to learn how smart credit card usage can lead to a significantly improved financial future.

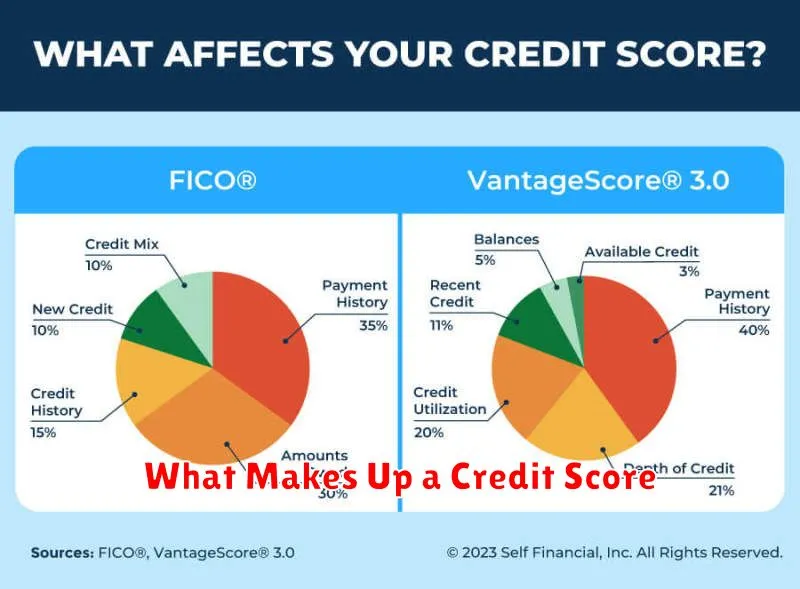

What Makes Up a Credit Score

Your credit score is a numerical representation of your creditworthiness, a key factor in determining your eligibility for loans, credit cards, and even some rental applications. It’s calculated using a complex formula, but understanding the key components can help you improve your score.

Payment History is the most significant factor, accounting for roughly 35% of your score. This reflects your track record of paying bills on time. Even one missed payment can negatively impact your score, so consistent on-time payments are crucial.

Amounts Owed, representing about 30% of your score, looks at how much debt you have relative to your available credit. This is often expressed as your credit utilization ratio. Keeping this ratio low (ideally below 30%) is essential for a good credit score. Using only a small portion of your available credit demonstrates responsible credit management.

Length of Credit History accounts for approximately 15% of your score. Lenders like to see a long and consistent history of responsible credit use. The older your accounts are, and the longer you’ve maintained them in good standing, the better your score will likely be.

New Credit comprises 10% of your score. Opening several new accounts in a short period can signal increased risk to lenders. It’s generally best to avoid applying for multiple credit accounts simultaneously.

Credit Mix makes up the remaining 10% of your score. Having a variety of credit accounts, such as credit cards and installment loans (like auto loans or mortgages), demonstrates a well-rounded approach to credit management. However, this factor carries less weight than the others.

Payment History and Timeliness

Your payment history is the single most important factor influencing your credit score. Lenders and credit bureaus meticulously track your repayment behavior across all your credit accounts. Consistent, on-time payments are crucial for building a strong credit profile.

Timeliness is key. Even a single missed or late payment can negatively impact your score, potentially for years. The severity of the impact depends on factors such as how late the payment was and the type of account involved. Multiple late payments will significantly damage your creditworthiness.

To ensure timely payments, consider setting up automatic payments for your credit cards. This eliminates the risk of forgetting due dates and ensures that your payments are always made on time. You can also use budgeting apps or calendar reminders to proactively manage your payment schedules.

Regularly review your credit card statements to confirm that all charges are accurate and that you understand the payment due date. Contact your credit card issuer immediately if you identify any discrepancies or anticipate difficulty making a payment on time. They may be able to offer solutions to avoid a late payment.

Maintaining a history of on-time payments across all your credit accounts consistently demonstrates your financial responsibility to lenders. This directly translates to a higher credit score and better chances of securing favorable credit terms in the future.

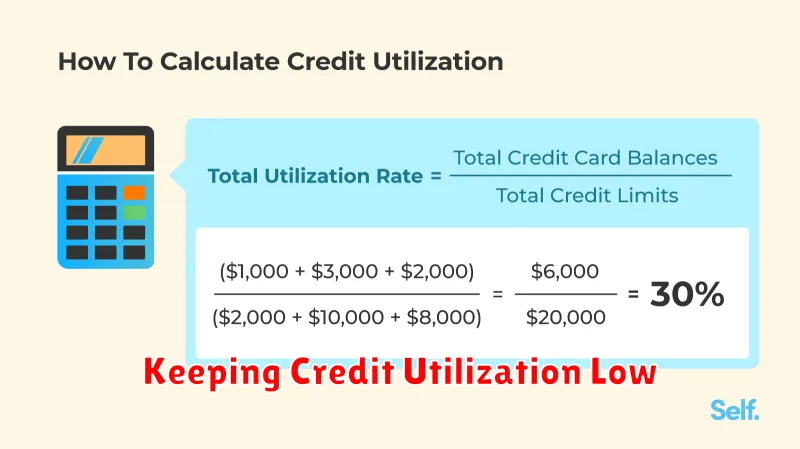

Keeping Credit Utilization Low

One of the most impactful factors affecting your credit score is your credit utilization ratio. This ratio represents the percentage of your available credit that you’re currently using. Lenders view a high credit utilization ratio as a sign of risk, suggesting you may be struggling to manage your finances.

To maintain a healthy credit score, strive to keep your credit utilization ratio below 30%. Ideally, aiming for under 10% is even better. This demonstrates responsible credit management and can significantly boost your creditworthiness. For example, if you have a total credit limit of $10,000, try to keep your outstanding balance below $3,000 (30%) or ideally, below $1,000 (10%).

There are several ways to lower your credit utilization. First, you can pay down existing balances on your credit cards. Regular payments, even small ones, will gradually reduce your outstanding debt. Secondly, consider increasing your credit limits. This can be done by requesting a credit limit increase from your existing card issuer, assuming you have a good payment history. However, be cautious not to overextend yourself financially. Remember, increasing your limit doesn’t automatically improve your credit score; responsible spending habits are key.

Regularly monitoring your credit report is crucial for tracking your credit utilization ratio and overall credit health. By staying informed and proactively managing your credit, you can effectively lower your utilization ratio and improve your credit score.

Avoiding Frequent New Applications

One of the most impactful factors affecting your credit score is the number of recent credit applications you’ve submitted. Each time you apply for a new credit card, loan, or other form of credit, a hard inquiry is made on your credit report. These inquiries can temporarily lower your score, as they signal increased risk to lenders.

Hard inquiries stay on your credit report for two years, though their impact diminishes over time. However, multiple inquiries within a short period indicate a potentially risky borrowing pattern, leading to a more significant negative effect on your creditworthiness. This is particularly true if you are applying for significant amounts of credit.

To mitigate this risk, carefully consider your need for new credit before applying. Only apply for credit when absolutely necessary, and avoid applying for multiple credit lines simultaneously. Instead, focus on responsible credit card usage with your existing cards to build a strong credit history. This responsible behavior, such as paying your bills on time and maintaining low credit utilization, will have a far more positive impact on your credit score than constantly applying for new cards.

Furthermore, understand that pre-approved or pre-qualified offers often don’t involve a hard inquiry. These offers often only perform a “soft inquiry,” which doesn’t negatively impact your credit score. However, even these should be approached judiciously to avoid creating the impression of excessive credit seeking.

In short, strategic application for new credit is key. Prioritize responsible credit management over the allure of numerous credit cards or loan offers. This will contribute significantly to improving and maintaining a healthy credit score.

How Long-Term Credit Accounts Help

Maintaining long-term credit accounts is a crucial factor in building a strong credit history. Lenders look favorably upon individuals who have demonstrated responsible credit management over an extended period. The length of your credit history, often referred to as your credit age, constitutes a significant portion of your credit score calculation.

Consistent and timely payments on long-term accounts significantly impact your payment history, a major component of your credit score. A long history of on-time payments showcases your reliability and financial responsibility to potential lenders. Conversely, missing payments, even on older accounts, can negatively affect your score.

Having a mix of different credit account types, including long-term accounts, also contributes positively to your credit profile. This diversification demonstrates your ability to manage various credit products responsibly. For instance, a long-standing credit card account alongside a mortgage or auto loan provides a well-rounded credit history, which is generally seen more favorably than having only one type of account.

Furthermore, long-term accounts often show lower credit utilization ratios over time. Credit utilization, the percentage of available credit used, is another critical factor in your credit score. As your credit limits increase on long-term accounts, and your spending habits remain responsible, your credit utilization ratio tends to decrease, which benefits your score.

In summary, establishing and maintaining long-term credit accounts, coupled with responsible credit management, is a strategic way to significantly improve and maintain a high credit score. The positive impact on your credit age, payment history, credit mix, and credit utilization is undeniable.

Using Alerts and Apps to Stay on Track

Effectively managing your credit score requires consistent monitoring and proactive measures. Leveraging alerts and mobile applications can significantly streamline this process, providing you with real-time insights into your credit health.

Many credit card companies offer account alerts that notify you via email or text message about crucial activities such as exceeding your credit limit, upcoming payments, and unusual account activity. Setting up these alerts ensures you’re promptly informed about potential issues, allowing you to take immediate corrective action. Consider configuring alerts for low balance notifications to prevent missed payments, a significant factor impacting your credit score.

Credit monitoring apps offer a more comprehensive overview of your credit standing. These apps often provide access to your credit report, credit score, and spending patterns. Some even offer features like budgeting tools and payment reminders, further enhancing your ability to manage your finances effectively. Regularly checking these apps allows you to identify and address any potential problems early, preventing them from negatively affecting your score.

The combination of account alerts from your credit card issuers and the features offered by credit monitoring apps empowers you to maintain a proactive approach to credit management. This proactive strategy, coupled with responsible spending habits, will contribute significantly towards improving and maintaining a healthy credit score.

{kind=link}