Are you dreaming of homeownership but unsure how mortgages work? Understanding the intricacies of a home loan is crucial for making informed financial decisions. This comprehensive guide, “How a Mortgage Works: Understanding Home Loans,” will demystify the process, equipping you with the knowledge to navigate the complexities of mortgage rates, loan terms, and the overall home-buying process. We’ll explore various mortgage types, helping you choose the best option for your individual circumstances and financial goals.

From the initial application and credit score assessment to closing costs and monthly payments, we’ll cover every aspect of securing a mortgage. Learn about pre-approval, down payments, and the importance of principal and interest. This guide offers clear explanations and practical advice, empowering you to make confident decisions as you embark on your journey towards owning a home. Prepare to gain a strong understanding of the entire mortgage process and the factors that influence your home loan.

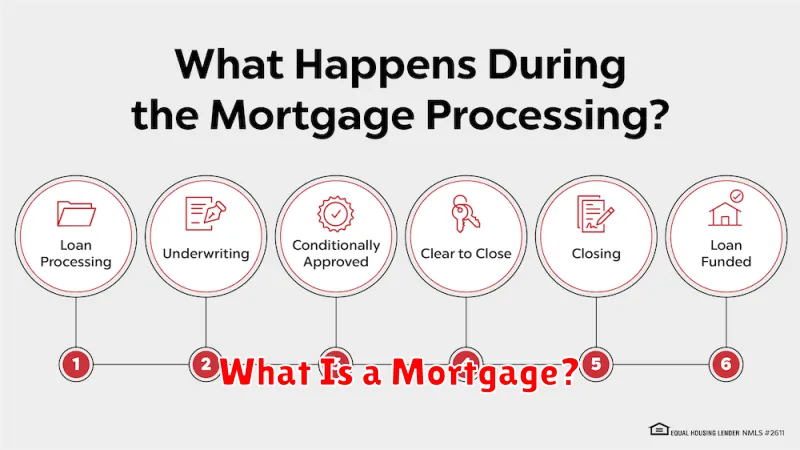

What Is a Mortgage?

A mortgage is a loan secured by real estate. It allows you to borrow a significant amount of money to purchase a home, with the property itself serving as collateral for the loan.

Essentially, you are borrowing money from a lender, typically a bank or other financial institution. In exchange for the funds, you agree to repay the loan over a specified period, typically 15 to 30 years, along with interest.

The interest rate is a crucial aspect of a mortgage. It represents the cost of borrowing the money, and it significantly impacts the total amount you will repay over the life of the loan. Interest rates fluctuate based on various economic factors.

If you fail to make your monthly mortgage payments, the lender has the right to foreclose on the property. This means they can legally seize and sell your home to recoup their losses.

Different types of mortgages exist, each with its own terms and conditions. These include fixed-rate mortgages, where the interest rate remains constant throughout the loan term, and adjustable-rate mortgages (ARMs), where the interest rate can change periodically based on market conditions. Understanding the nuances of each type is vital before committing to a mortgage.

Obtaining a mortgage usually requires a thorough application process, involving credit checks, income verification, and appraisal of the property. A strong credit history and a stable financial situation are generally necessary to qualify for favorable mortgage terms.

Fixed vs Adjustable Rates

Choosing between a fixed-rate and an adjustable-rate mortgage (ARM) is a crucial decision when securing a home loan. Understanding the core differences between these two options is essential for making an informed choice that aligns with your financial goals and risk tolerance.

A fixed-rate mortgage offers predictability and stability. The interest rate remains constant for the entire loan term, typically 15 or 30 years. This means your monthly payments will be the same throughout the life of the loan, allowing for easier budgeting and financial planning. While offering certainty, fixed-rate mortgages may have a slightly higher initial interest rate compared to ARMs.

Conversely, an adjustable-rate mortgage (ARM) features an interest rate that fluctuates over time. The rate is typically fixed for an initial period, often 5 or 7 years (the initial adjustment period), after which it adjusts periodically based on a market index, such as the LIBOR or a similar benchmark. This means your monthly payments could increase or decrease depending on market interest rate movements. While potentially offering a lower initial interest rate, ARMs carry greater risk due to the uncertainty of future payments. Understanding the index used, the margin added to the index, and the adjustment frequency is vital before selecting an ARM.

The best choice between a fixed-rate and an adjustable-rate mortgage depends heavily on individual circumstances and predictions about future interest rates. Factors to consider include your risk tolerance, the length of time you plan to stay in the home, and your overall financial stability.

Down Payments and Loan-to-Value Ratios

A down payment is the initial upfront payment you make when purchasing a home. It’s the portion of the home’s purchase price that you pay out-of-pocket, and it’s typically expressed as a percentage of the total price. For example, a 20% down payment on a $300,000 home would be $60,000.

The size of your down payment significantly impacts several aspects of your mortgage. A larger down payment generally results in a lower loan amount, leading to lower monthly payments and potentially a lower interest rate. It also reduces your loan-to-value ratio (LTV), which is a crucial factor lenders consider when assessing your risk.

The loan-to-value ratio (LTV) is calculated by dividing the loan amount by the appraised value of the home. For instance, with a $240,000 loan on a $300,000 home, the LTV is 80% (240,000 / 300,000 = 0.80). A lower LTV generally means less risk for the lender, as they have a larger cushion in case the home’s value decreases. This can translate to more favorable mortgage terms.

Different lenders have varying requirements for minimum down payments and maximum LTVs. Conventional loans often require a minimum down payment of 3% to 20%, while FHA loans, designed for first-time homebuyers, may allow for significantly lower down payments, sometimes as low as 3.5%. However, lower down payments often come with higher interest rates and potentially added fees, such as private mortgage insurance (PMI).

Understanding the interplay between down payments and LTV ratios is crucial for securing a mortgage that aligns with your financial capabilities and goals. Carefully assess your financial situation and consult with a mortgage professional to determine the best strategy for your individual circumstances.

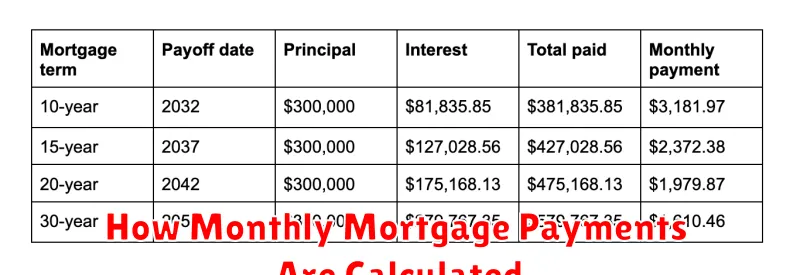

How Monthly Mortgage Payments Are Calculated

Understanding how your monthly mortgage payment is calculated is crucial for responsible homeownership. The process involves several key factors, primarily your loan amount, interest rate, and loan term (the length of your mortgage).

The most common method used to calculate mortgage payments is the amortization formula. This formula considers the principle balance (the amount you borrowed), the interest rate (typically expressed as an annual percentage rate or APR), and the loan term (usually in months). It calculates a fixed monthly payment that covers both the principal (the actual amount of the loan) and the interest accrued on the outstanding balance.

The formula itself is somewhat complex, but it essentially involves calculating the present value of a series of future payments. Lenders use sophisticated software or financial calculators to apply this formula accurately. However, understanding the core components is key to grasping your mortgage payment. A higher interest rate will result in a larger monthly payment, as will a longer loan term (although the total interest paid over the life of the loan will be higher with a longer term). A larger loan amount naturally leads to a higher monthly payment as well.

In addition to principal and interest, your monthly payment typically includes property taxes and homeowner’s insurance. These are often bundled into your monthly payment through a process called escrow. Your lender collects these funds and pays the taxes and insurance on your behalf. This simplifies your financial obligations but adds to your overall monthly mortgage payment.

Finally, you may also encounter additional fees such as private mortgage insurance (PMI) if your down payment is less than 20% of the home’s purchase price, or points which are upfront fees that can reduce your interest rate. These fees, if applicable, will be factored into your total monthly payment.

What Escrow Is and Why It Matters

In the context of a mortgage, escrow is a crucial process where your lender holds funds on your behalf to pay certain recurring expenses associated with your homeownership. This eliminates the need for you to make separate payments for these items, streamlining your financial responsibilities.

Typically, your monthly mortgage payment includes not only your principal and interest but also a portion allocated to your escrow account. This account is managed by your lender and funds are used to pay your property taxes and homeowner’s insurance premiums. Some lenders may also include private mortgage insurance (PMI) payments in escrow.

The importance of escrow lies in its role in protecting both you and your lender. For you, it simplifies the payment process, ensuring that your taxes and insurance are paid on time, preventing potential late fees or penalties. For your lender, it guarantees that the property remains adequately insured and the taxes are current, safeguarding their investment.

Your lender will usually estimate the annual amount needed for taxes and insurance based on your property’s assessed value and your insurance policy. They then divide this amount by twelve to determine your monthly escrow payment. It’s important to note that your escrow payment might adjust periodically to reflect changes in your property taxes or insurance premiums.

Understanding the mechanics of escrow is vital for responsible homeownership. It’s advisable to regularly review your escrow account statements to ensure accuracy and to address any discrepancies promptly with your lender. This proactive approach will help maintain smooth financial management throughout the life of your mortgage.

Steps to Get Approved for a Home Loan

Securing a home loan involves a multi-step process that requires careful planning and preparation. The first step is to assess your financial situation. This includes checking your credit score, understanding your debt-to-income ratio (DTI), and determining how much you can comfortably afford to borrow. A strong credit score and a low DTI significantly improve your chances of approval.

Next, you’ll need to shop around for a mortgage lender. Different lenders offer various loan programs with different interest rates and terms. Comparing offers from multiple lenders helps you find the best option for your financial needs. Consider factors such as interest rates, loan fees, and the lender’s reputation.

Once you’ve chosen a lender, you’ll need to complete a loan application. This application will require extensive personal and financial information, including your income, employment history, assets, and debts. Be prepared to provide supporting documentation such as pay stubs, tax returns, and bank statements to verify the information you provide.

After submitting your application, the lender will conduct a thorough review of your financial information. This process may involve a credit check, appraisal of the property you intend to purchase, and verification of your employment and income. Be prepared for a lengthy underwriting process, which can take several weeks or even months.

Finally, if your application is approved, you’ll receive a loan commitment from the lender. This commitment outlines the terms of your loan, including the interest rate, loan amount, and monthly payments. At this stage, you’ll typically need to finalize the closing process, which involves signing loan documents and paying closing costs.

{kind=link}