Are you considering applying for a personal loan but unsure where to start? Understanding the basics of a personal loan is crucial before you commit to borrowing money. This comprehensive guide will equip you with the knowledge you need to navigate the process confidently, from determining your eligibility and comparing interest rates to choosing the best loan term and managing repayments. We’ll cover everything you need to know to secure a personal loan that meets your financial needs and avoids potential pitfalls.

This article will delve into the key aspects of personal loans, clarifying the different types available, explaining the application process, and highlighting the importance of responsible borrowing. We will explore essential factors to consider such as credit score impact, fees and charges, and the various repayment options. Whether you’re looking to consolidate debt, finance a home improvement project, or cover unexpected expenses, this guide will provide you with a clear understanding of how personal loans work and help you make informed decisions about your finances. Learn how to obtain the best personal loan for your circumstances.

What Is a Personal Loan and How It Works

A personal loan is a type of unsecured loan that you can use for various purposes, such as debt consolidation, home improvements, or medical expenses. Unlike secured loans, which require collateral (like a car or house), personal loans are based on your creditworthiness.

The process typically begins with applying for a loan from a bank, credit union, or online lender. You’ll need to provide information about your income, credit history, and the purpose of the loan. The lender will then review your application and determine whether to approve you, and if so, at what interest rate and loan term.

Once approved, you’ll receive the loan amount in a lump sum. You’ll then repay the loan, plus interest, in fixed monthly installments over the agreed-upon loan term. The monthly payment amount is determined by the loan amount, interest rate, and loan term. Shorter loan terms typically result in higher monthly payments but lower overall interest costs, while longer loan terms result in lower monthly payments but higher overall interest costs.

Interest rates on personal loans vary depending on several factors, including your credit score, income, debt-to-income ratio, and the lender. It’s important to shop around and compare offers from different lenders to find the best interest rate and terms.

A key aspect to consider is the Annual Percentage Rate (APR). This represents the total cost of the loan, including interest and any fees. A lower APR indicates a less expensive loan.

Before taking out a personal loan, carefully review the loan agreement and understand all the terms and conditions. Make sure you can comfortably afford the monthly payments without straining your budget.

Types of Personal Loans: Secured vs Unsecured

Personal loans are broadly categorized into two main types: secured and unsecured. The key difference lies in whether the loan requires collateral.

A secured personal loan requires you to pledge an asset, such as a car or a house, as collateral. If you fail to repay the loan, the lender can seize and sell the collateral to recover their losses. Secured loans typically offer lower interest rates because the lender has less risk.

In contrast, an unsecured personal loan does not require any collateral. These loans are based solely on your creditworthiness. Lenders assess your credit score, income, and debt-to-income ratio to determine your eligibility and the interest rate. Because the lender assumes more risk, unsecured loans usually carry higher interest rates than secured loans.

The choice between a secured and unsecured personal loan depends on your individual financial situation and risk tolerance. If you have valuable assets you’re willing to put at risk, a secured loan might offer a more favorable interest rate. However, if you prefer to protect your assets, an unsecured loan might be a better option, even if it comes with a higher interest rate.

It is crucial to carefully consider the terms and conditions of any loan before accepting it, regardless of whether it is secured or unsecured. Understanding the interest rate, repayment schedule, and any associated fees will help you make an informed decision.

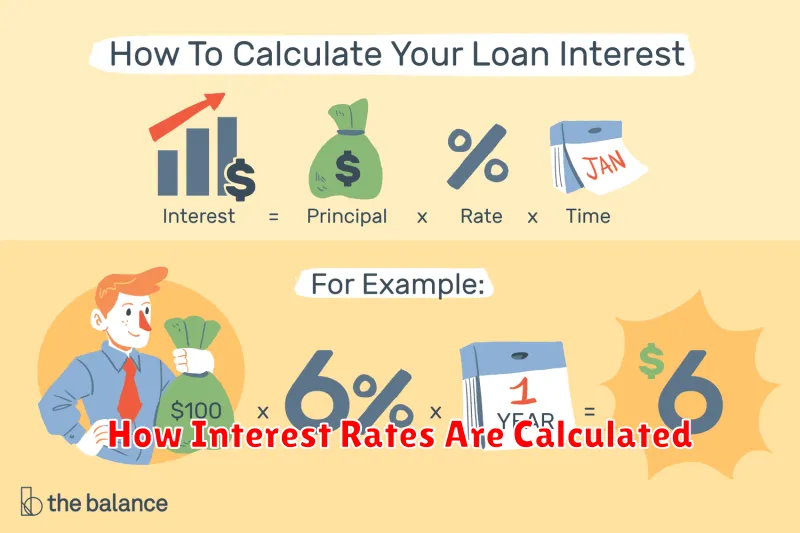

How Interest Rates Are Calculated

Understanding how interest rates are calculated is crucial when considering a personal loan. The calculation itself isn’t overly complex, but the factors influencing the rate can be numerous and vary significantly between lenders.

The most fundamental aspect is the annual percentage rate (APR). This represents the total cost of borrowing, including the interest rate and any other fees associated with the loan. It’s expressed as a yearly percentage and is a vital tool for comparing different loan offers.

While the interest rate itself is a key component of the APR, its calculation is often based on a combination of factors. These typically include the borrower’s credit score, the loan amount, the loan term, and the lender’s risk assessment. A higher credit score generally results in a lower interest rate, as it indicates a lower risk of default for the lender.

The loan term also plays a significant role. Longer loan terms typically lead to lower monthly payments, but the total interest paid over the life of the loan will be higher due to the extended repayment period. Conversely, shorter loan terms result in higher monthly payments but lower overall interest charges.

Finally, the lender’s risk assessment takes into account various factors beyond the borrower’s credit score. This might include the purpose of the loan, the borrower’s income and debt levels, and the overall economic climate. Lenders use sophisticated models to assess these risks, which in turn influences the interest rate offered.

Repayment Terms and Monthly Installments

Understanding the repayment terms of a personal loan is crucial before you sign the agreement. These terms outline the timeframe you have to repay the loan, typically expressed in months or years. A longer repayment period will result in lower monthly installments, but you’ll end up paying more in interest over the life of the loan. Conversely, a shorter repayment period means higher monthly payments but less overall interest paid.

Your monthly installment is the fixed amount you’ll pay each month until the loan is fully repaid. This amount is calculated based on the loan amount, the interest rate, and the repayment term. It’s essential to ensure your monthly payment fits comfortably within your budget. Failing to make timely payments can negatively impact your credit score and result in additional fees.

Before agreeing to a loan, carefully review the amortization schedule. This schedule provides a detailed breakdown of each monthly payment, showing how much goes towards principal repayment and how much goes towards interest. This allows you to visualize how your loan balance decreases over time. Pay close attention to the Annual Percentage Rate (APR), which reflects the total cost of borrowing, including interest and fees.

Remember to consider the implications of different repayment terms and their effect on your overall finances. Choosing a repayment term that balances affordability with minimizing total interest paid is a key aspect of responsible borrowing.

How Personal Loans Impact Credit Scores

A personal loan can significantly impact your credit score, both positively and negatively, depending on how you manage it. The effects are primarily seen through the changes in your credit report.

Positive impacts occur when you consistently make on-time payments. Each on-time payment contributes to your payment history, a crucial factor in determining your credit score. This demonstrates responsible borrowing behavior to lenders, resulting in a gradual increase in your credit score over time. Additionally, taking out a personal loan and managing it well can actually help build credit, particularly if you have a limited credit history.

Conversely, negative impacts arise from missed or late payments. Late or missed payments significantly lower your credit score, as they indicate to lenders a higher risk of default. This negative mark stays on your credit report for a considerable amount of time, making it harder to obtain future credit and potentially resulting in higher interest rates. Furthermore, frequently applying for personal loans in a short period can also negatively affect your credit score, as lenders view multiple applications as a sign of financial instability.

The amount of credit you utilize also plays a role. Utilizing a large portion of your available credit (high credit utilization) can lower your credit score. Responsible use of personal loan credit involves maintaining a low credit utilization ratio. Therefore, borrowing responsibly and repaying the loan promptly minimizes negative impacts.

In summary, a personal loan’s effect on your credit score is directly tied to your ability to manage it effectively. Careful planning, budgeting, and consistent on-time payments are crucial to ensuring a positive impact on your credit profile.

Questions to Ask Before Taking a Loan

Securing a personal loan is a significant financial decision. Before committing, it’s crucial to ask yourself—and your lender—several key questions to ensure the loan aligns with your financial goals and capabilities. Understanding the terms thoroughly will help avoid future difficulties.

What is the total cost of the loan? This encompasses not only the principal amount but also all associated fees, including origination fees, processing fees, and any potential prepayment penalties. Calculating the Annual Percentage Rate (APR) is essential for comparing different loan offers effectively.

What is the repayment schedule? Understanding the loan’s term length and the monthly payment amount is vital. Ensure the monthly payments fit comfortably within your budget without compromising your other financial obligations. Inquire about the possibility of making extra payments and if there are any associated penalties or benefits.

What are the eligibility requirements? Confirm you meet all the lender’s criteria before proceeding. This includes credit score requirements, income verification processes, and any collateral requirements. Understanding these aspects upfront saves time and potential disappointment.

What happens if I miss a payment? Late payment fees and their potential impact on your credit score must be thoroughly understood. Inquire about the lender’s policies concerning late or missed payments and explore options for managing financial difficulties.

What are the lender’s customer service policies? A reputable lender provides clear communication channels and readily available support. Understanding their procedures for addressing concerns or resolving disputes is vital for a positive borrowing experience.

Are there any hidden fees or clauses? Carefully review the loan agreement for any hidden costs or unfavorable terms that might not be immediately apparent. Don’t hesitate to ask for clarification on any confusing aspects of the contract.

Asking these critical questions empowers you to make an informed decision, securing a loan that benefits your financial well-being rather than causing future stress.

When Personal Loans Are a Useful Tool

Personal loans can be a valuable financial tool in a variety of situations. They offer a structured way to borrow a specific amount of money, repayable over a set period with fixed interest payments. This predictability can be incredibly helpful for managing your finances.

One common use is for consolidating debt. If you have multiple high-interest debts, such as credit cards, a personal loan can help you combine them into a single, lower-interest payment. This simplifies your finances and can potentially save you money on interest over time.

Large unexpected expenses, like significant home repairs or unexpected medical bills, can be easily managed with a personal loan. Instead of relying on high-interest credit cards or depleting savings, a personal loan provides a more manageable and affordable payment plan.

Major purchases, such as a new appliance or furniture, can also be financed through a personal loan. This allows you to spread the cost over several months or years, making a large purchase more affordable and preventing the need to put significant strain on your current budget.

Furthermore, personal loans can be used for home improvements that enhance the value of your property. This is a strategic way to finance upgrades without immediately impacting your savings or increasing your overall debt burden excessively.

Finally, financing education or starting a small business are also viable uses for personal loans. While other financing options might exist, a personal loan can offer flexibility and control over repayment terms. However, it’s crucial to carefully assess the financial implications before utilizing a personal loan for these purposes.

{kind=link}