Are you trapped in a cycle of credit card debt? Do you find yourself constantly paying minimum payments, only to see your balance remain stubbornly high? The credit card debt spiral is a dangerous trap that can significantly impact your financial health and overall well-being. This article will provide you with practical strategies to break free from the cycle and regain control of your finances. We’ll explore effective techniques to manage high-interest debt, create a realistic budget, and build healthy spending habits to prevent future debt accumulation. Learn how to avoid the pitfalls of credit card debt and pave the way towards financial freedom.

Understanding how to navigate the complexities of credit card payments is crucial to avoiding a debilitating debt spiral. We will delve into the mechanics of interest rates and APR (Annual Percentage Rate), showing you how these factors contribute to the rapid growth of your debt. We’ll also discuss different debt management strategies, including debt consolidation, balance transfers, and negotiating with creditors. This comprehensive guide empowers you to take control of your finances and make informed decisions to achieve long-term financial stability. Avoid the credit card debt spiral and reclaim your financial future.

What Is the Credit Card Debt Spiral?

The credit card debt spiral is a vicious cycle where high interest charges on outstanding balances make it increasingly difficult to pay down debt. It’s characterized by a continuous pattern of minimum payments, accruing interest, and ultimately, increasing the total amount owed.

The spiral begins when you only make the minimum payment on your credit card each month. While this might seem manageable initially, the majority of your payment goes towards interest, leaving only a small fraction applied to the principal balance. This means that you are essentially paying interest on interest, leading to slow, or nonexistent, progress toward eliminating the debt.

As the balance remains high, the interest charges accumulate rapidly. This results in a higher minimum payment each month, making it even harder to make significant headway against the principal balance. Eventually, the minimum payment becomes a substantial portion of your monthly budget, restricting your ability to save, invest, or address other financial obligations.

Furthermore, the high interest rates associated with credit cards exacerbate the problem. Even small purchases can quickly snowball into significant debt, particularly if you consistently rely on credit to cover expenses. The relentless accumulation of interest creates a sense of hopelessness, making it increasingly challenging to break free from the cycle.

The consequences of the credit card debt spiral can be severe, including damaged credit scores, stress, and financial instability. Understanding the mechanics of this cycle is the crucial first step in developing effective strategies to avoid it.

Warning Signs to Watch Out For

One of the most insidious aspects of credit card debt is its gradual, almost imperceptible creep. Ignoring early warning signs can quickly lead to a spiraling debt situation that’s difficult to escape. Paying close attention to your spending habits and credit reports is crucial for preventing this.

A significant increase in your credit card balances month-over-month, especially without a corresponding increase in income, should raise a red flag. This suggests you’re spending more than you can comfortably repay each month, and you’re likely relying on carrying a balance.

Difficulty making minimum payments on time is another major warning sign. Even if you’re making the minimum payment, consistently struggling to meet that obligation signals an unsustainable level of debt. Missed payments, even one, can severely impact your credit score and further exacerbate the problem.

Using credit cards to pay for essential expenses like rent, groceries, or utilities is a serious indicator that you’re in over your head. This implies that your income isn’t sufficient to cover your basic needs, and relying on credit to compensate creates a vicious cycle of debt.

Feeling anxious or stressed about your credit card bills is a common emotional symptom of a growing debt problem. If you consistently dread opening your credit card statements or avoid thinking about your outstanding balances, it’s a sign you need to take immediate action.

Finally, noticeably decreased savings or a dwindling emergency fund should serve as a clear warning. Having little to no savings makes it incredibly difficult to manage unexpected expenses, potentially leading to further reliance on credit cards and a worsening debt situation.

The Danger of Only Paying the Minimum

Many people believe that paying only the minimum payment on their credit cards is a viable strategy for managing debt. This couldn’t be further from the truth. While it may seem like a small, manageable amount each month, this approach is a dangerous path leading to a credit card debt spiral.

The primary danger lies in the high interest rates associated with credit cards. When you only pay the minimum, a significantly larger portion of your payment goes towards interest, rather than the principal balance. This means you’re essentially paying more for the privilege of borrowing the money, extending your repayment period, and increasing the total amount you end up paying.

Consider this: A significant portion of your monthly payment is absorbed by interest, leaving only a small amount to reduce the actual debt. This results in a slow, agonizing repayment process, allowing the interest to continue to accumulate and further inflate the balance. Over time, the interest charges can easily outweigh the initial debt itself.

Furthermore, consistently making only minimum payments can negatively impact your credit score. Lenders view this behavior as a sign of financial instability and risk, leading to a lower credit score which makes securing future loans or favorable interest rates significantly harder. The resulting financial repercussions can have long-term consequences.

In short, while paying the minimum may provide short-term relief, it’s a financially unsustainable practice. It’s a trap that leads to increased debt, higher interest payments, and damaged creditworthiness. A more proactive approach to debt management is crucial to avoid this dangerous cycle.

Avoiding Multiple Card Dependence

One of the most crucial steps in preventing a credit card debt spiral is to avoid becoming overly reliant on multiple credit cards. While having a couple of cards can offer benefits like rewards programs and different spending options, juggling numerous cards significantly increases the risk of losing track of payments, interest rates, and due dates.

The complexity of managing multiple accounts can lead to missed payments, which trigger late fees and negatively impact your credit score. Further, higher interest rates on some cards can quickly escalate your debt, particularly if you’re only making minimum payments. The more cards you have, the more opportunities there are for this to happen.

Instead of accumulating numerous cards, focus on effectively managing one or two. Choose cards that align with your spending habits and offer rewards that are beneficial to you. This approach simplifies your financial life, making it easier to stay organized and avoid the pitfalls of overspending.

Regularly review your credit card statements for all your cards to monitor your spending and ensure that you’re making timely payments. Consider using budgeting apps or spreadsheets to track your spending across all accounts. This proactive approach can help prevent you from overextending yourself financially and spiraling into debt.

If you already have several credit cards and are struggling to manage them, consider consolidating your debt onto a single card with a lower interest rate, or exploring other debt management options. This strategic move can simplify your financial situation and provide a path towards a debt-free future.

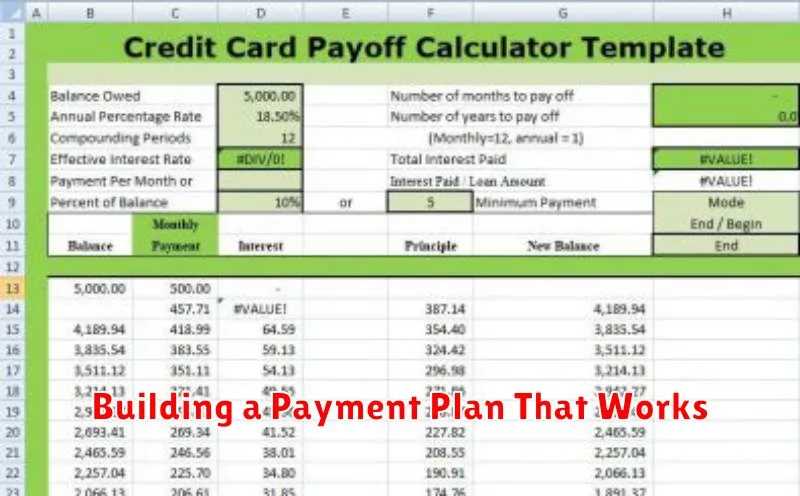

Building a Payment Plan That Works

Facing significant credit card debt can feel overwhelming, but creating a manageable payment plan is crucial to breaking free from the debt spiral. The key is to develop a plan that’s both realistic and effective, tailored to your individual financial situation.

Begin by listing all your credit cards, noting each balance, interest rate, and minimum payment. This provides a clear picture of your overall debt. Next, determine your monthly disposable income – the money left after essential expenses like rent, utilities, and groceries. This figure will dictate how much you can realistically allocate towards debt repayment.

Consider different repayment strategies. The debt avalanche method focuses on paying off the highest-interest debt first, regardless of balance. This minimizes the total interest paid over time. Alternatively, the debt snowball method prioritizes paying off the smallest debt first for psychological motivation, then rolling that payment amount into the next smallest debt. The choice depends on your personal preferences and financial discipline.

Once you’ve chosen a method, build your payment plan. Allocate as much of your disposable income as possible to debt repayment, prioritizing the targeted card(s). While aiming for more than the minimum payment is ideal, ensure the plan is sustainable to avoid further financial stress. Regularly monitor your progress and adjust the plan as needed. Life circumstances change, and your payment plan should adapt accordingly.

Seek professional help if needed. A credit counselor can offer guidance, negotiation with creditors, and potentially consolidate your debt into a single, lower-interest payment. Remember, tackling debt is a journey, not a sprint. Consistency and a well-structured plan are essential for success.

Why Balance Transfers Aren’t Always the Answer

While a balance transfer can seem like a quick fix for overwhelming credit card debt, it’s crucial to understand that it’s not a one-size-fits-all solution. In fact, for many, it can exacerbate the problem if not approached carefully.

One major drawback is the balance transfer fee. Many credit cards charge a percentage of the balance transferred, often around 3-5%. This fee immediately reduces the amount of debt you actually eliminate. If you’re only transferring a small portion of your debt, the fee might outweigh any interest savings.

Another significant factor is the introductory period. Balance transfer offers often include a period of 0% APR, but this is typically temporary, usually lasting only 6-18 months. After this period expires, the interest rate can skyrocket, potentially exceeding your original card’s rate. Failing to pay down a significant portion of the debt during the introductory period can lead to a much higher interest burden.

Furthermore, opening a new credit card for a balance transfer can negatively impact your credit score. Each new credit application results in a hard inquiry, which can temporarily lower your score. Additionally, increasing your available credit can potentially increase your credit utilization ratio (the amount of credit you use compared to your total available credit), which is a significant factor in your credit score. A higher utilization ratio can also negatively impact your score.

Finally, the psychology of debt shouldn’t be underestimated. A balance transfer can create a false sense of security, delaying the necessary steps towards true financial responsibility. Without addressing the underlying spending habits that led to the debt in the first place, the cycle of debt will likely continue, even with a balance transfer.

{kind=link}