Are you in the market for a personal loan but feeling overwhelmed by the sheer number of offers available? Navigating the world of loan interest rates, fees, and repayment terms can be daunting. This comprehensive guide, “How to Compare Personal Loan Offers Like a Pro,” will equip you with the essential strategies and knowledge to confidently compare personal loan options and secure the most favorable terms for your financial needs. We’ll break down the key factors to consider, providing you with a clear, step-by-step approach to ensure you make an informed decision and avoid costly mistakes.

Choosing the right personal loan can significantly impact your financial well-being. Understanding the nuances of APR (Annual Percentage Rate), loan origination fees, and prepayment penalties is crucial for making a smart choice. This article will empower you to become a savvy borrower, enabling you to compare multiple lenders, analyze their offers effectively, and ultimately, select the best personal loan that aligns with your budget and financial goals. Learn how to avoid hidden costs and secure a competitive interest rate with our expert advice.

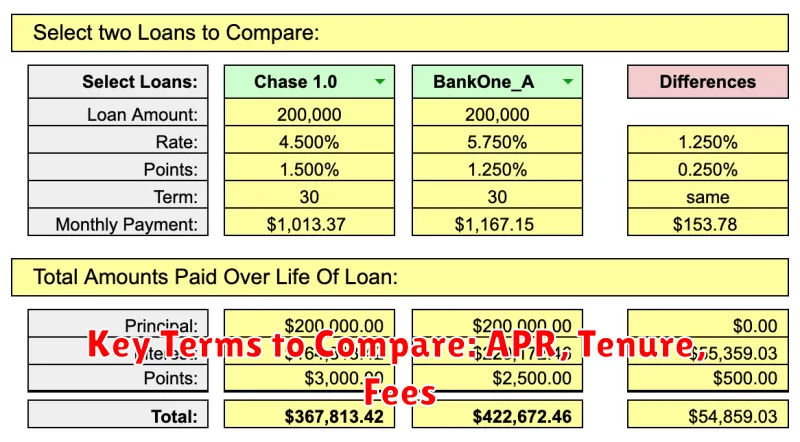

Key Terms to Compare: APR, Tenure, Fees

When comparing personal loan offers, understanding a few key terms is crucial for making an informed decision. These terms directly impact the overall cost and affordability of your loan. Let’s examine three essential factors: Annual Percentage Rate (APR), tenure, and fees.

Annual Percentage Rate (APR) represents the total cost of borrowing, including interest and any other fees expressed as a yearly percentage. A lower APR generally indicates a less expensive loan. It’s vital to compare APRs across different offers, as even small differences can significantly affect the total amount repaid over the life of the loan. Make sure to carefully examine the APRs before making a choice.

Tenure, also known as the loan term, refers to the length of time you have to repay the loan. This is typically expressed in months or years. A shorter tenure will mean higher monthly payments but lower overall interest costs due to less time accruing interest. Conversely, a longer tenure leads to lower monthly payments but higher overall interest costs because of the extended repayment period. Consider your budget and financial goals when determining the most suitable tenure.

Fees associated with personal loans can vary significantly. These might include originating fees, prepayment penalties, or late payment fees. Carefully review the loan agreement to understand all applicable fees. While seemingly small, these fees can add up over time and dramatically impact the total cost of the loan. Compare fees across different offers to identify the most cost-effective option.

Understanding Total Repayment Over Time

When comparing personal loan offers, it’s crucial to understand the total repayment amount. This figure represents the sum of all payments you’ll make over the loan’s lifetime, including both the principal (the original loan amount) and the interest.

A lower total repayment amount indicates a more cost-effective loan. While a lower monthly payment might seem attractive, it could mean a longer repayment period and ultimately higher total interest paid. Therefore, always compare the total repayment amount across different offers, not just the monthly installments.

To calculate the total repayment amount, you can use a loan amortization calculator or manually add up the monthly payments outlined in the loan agreement. This involves considering the loan term (length of the loan) and the interest rate. A longer loan term generally leads to a higher total repayment amount due to accumulating interest over a longer period.

Carefully reviewing the Annual Percentage Rate (APR) also helps determine the total repayment cost. The APR incorporates all loan fees and interest, giving you a more accurate picture of the total cost of borrowing. A lower APR generally translates to a lower total repayment amount.

By focusing on the total repayment amount, you can make an informed decision and choose the personal loan that offers the best value for your money, minimizing the overall cost of borrowing.

Fixed vs Variable Interest Rates

Understanding the difference between fixed and variable interest rates is crucial when comparing personal loan offers. This choice significantly impacts your overall loan cost.

A fixed interest rate remains constant throughout the loan term. This predictability offers stability; your monthly payment will not change, making budgeting easier. Knowing the exact amount you’ll pay each month eliminates surprises and provides financial certainty.

Conversely, a variable interest rate fluctuates based on market conditions. This means your monthly payment can increase or decrease over the life of the loan. While you might benefit from lower payments initially if interest rates fall, you also risk facing higher payments if rates rise. This uncertainty can make budgeting challenging.

The best choice depends on your individual circumstances and risk tolerance. If you prioritize predictability and want a consistent monthly payment, a fixed-rate loan is generally preferred. However, if you believe interest rates are likely to decline, a variable-rate loan might offer potential savings, but with increased risk.

Carefully consider your financial situation and long-term outlook when making this critical decision. Don’t hesitate to consult with a financial advisor for personalized guidance.

Watch for Hidden Fees and Clauses

Before committing to a personal loan, meticulously examine the terms and conditions for any hidden fees or unfavorable clauses. Lenders sometimes bury important details within lengthy documents, making it easy to overlook significant costs.

Pay close attention to fees such as origination fees, prepayment penalties, and late payment fees. Understand how these fees are calculated and their potential impact on your overall loan cost. A seemingly low interest rate can be offset by substantial hidden charges.

Carefully review clauses relating to interest rate adjustments, automatic payments, and dispute resolution. Some loans might contain clauses allowing for interest rate increases without prior notice, or impose penalties for missed or late payments that are significantly higher than initially stated.

Don’t hesitate to contact the lender directly if any aspect of the terms and conditions is unclear. A reputable lender should be happy to explain all fees and clauses transparently. If you encounter resistance or evasiveness, it might be a red flag warranting further investigation or considering alternative loan offers.

Comparing loan offers solely based on the advertised interest rate is insufficient. A comprehensive comparison must include all applicable fees and a thorough understanding of the associated terms and conditions. This diligent approach will ensure you secure the most cost-effective personal loan.

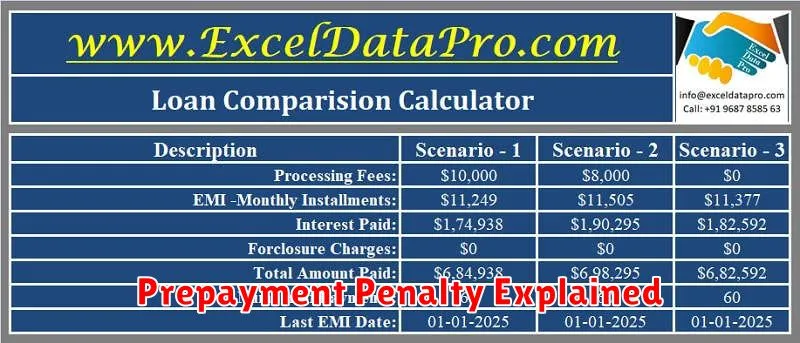

Prepayment Penalty Explained

A prepayment penalty is a fee charged by a lender when you pay off your personal loan before its scheduled maturity date. This penalty compensates the lender for lost interest income they would have earned had you continued making payments according to the original loan agreement.

The amount of the prepayment penalty can vary significantly depending on the lender and the terms of your loan. Some lenders may charge a fixed percentage of the remaining loan balance, while others may use a more complex calculation. It’s crucial to carefully review your loan agreement to understand the specific terms and conditions related to prepayment penalties. Understanding this fee is vital before signing any loan documents.

Many personal loans do not include prepayment penalties, particularly those offered by online lenders or credit unions. However, it’s essential to confirm the absence of such a fee before proceeding with your loan application. If a penalty applies, consider the potential cost versus the benefits of paying off the loan early. You may wish to factor this into your decision-making process.

Always inquire about prepayment penalties during the loan application process. Don’t hesitate to ask specific questions about the calculation method, the amount of the penalty, and the conditions under which it applies. Clear communication with your lender ensures you understand all aspects of the loan agreement before committing to it.

Comparing loans with and without prepayment penalties is a critical aspect of securing the best deal. While a lower interest rate may seem attractive, a significant prepayment penalty could negate any savings if you anticipate paying the loan off early.

Checklist Before Choosing a Lender

Before committing to a personal loan, it’s crucial to thoroughly vet potential lenders. A comprehensive checklist will help ensure you’re making an informed decision and securing the best possible terms.

First, verify the lender’s reputation and legitimacy. Check online reviews and ratings from reputable sources to gauge customer satisfaction and identify any red flags. Look for indicators of transparency and a history of ethical practices. Investigate whether they’re licensed and regulated in your jurisdiction. Confirming their financial stability is also vital; a lender’s stability directly impacts your loan’s security.

Next, carefully compare interest rates and fees. Don’t focus solely on the advertised rate. Scrutinize the Annual Percentage Rate (APR), which includes all fees and charges, offering a more complete picture of the actual cost. Be aware of origination fees, prepayment penalties, and late payment fees. Understanding these costs is vital for accurately comparing loan offers.

Examine the loan’s terms and conditions. Pay close attention to the repayment schedule, including the loan’s duration and the frequency of payments. Consider whether a fixed or variable interest rate best suits your financial situation and risk tolerance. Also, ensure you clearly understand the loan’s eligibility requirements and any potential consequences of default.

Finally, assess the lender’s customer service. A responsive and helpful customer service team can be invaluable, especially if you encounter any issues during the loan process. Look for lenders who offer multiple channels for communication, such as phone, email, and online chat. A positive customer experience can significantly enhance your borrowing experience.

{kind=link}