Understanding the psychology of personal loans is crucial for both borrowers and lenders. This article delves into the often-overlooked behavioral aspects of borrowing money, exploring how taking out a personal loan can significantly impact financial behavior. We’ll examine the psychological effects of debt, including the potential for increased stress and altered decision-making processes. Learn how understanding these psychological mechanisms can help you make more informed decisions regarding personal finance and avoid the pitfalls of irresponsible borrowing.

From the initial thrill of accessing readily available funds to the long-term implications of debt management, the emotional and cognitive aspects of personal loan usage are complex. We will analyze the influence of marketing strategies, cognitive biases, and individual financial literacy on borrowing habits. Discover how to mitigate the negative impacts of debt, develop healthier financial planning strategies, and cultivate responsible borrowing behaviors. This insightful exploration will equip you with the knowledge to navigate the psychological landscape of personal loans successfully.

How Debt Changes the Way We View Money

The accumulation of debt fundamentally alters our relationship with money, often shifting our perspective from one of abundance and opportunity to one characterized by scarcity and anxiety. This change isn’t simply a matter of having less disposable income; it’s a deeper psychological shift impacting our financial decision-making processes and overall well-being.

When we’re free from significant debt, money often feels like a resource to be utilized for achieving goals – whether that’s saving for a down payment, investing in education, or enjoying leisure activities. The psychological experience is one of control and agency. We feel empowered to make choices based on our desires and aspirations.

However, under the weight of debt, this perspective can dramatically change. The focus shifts from pursuing future goals to managing present obligations. The constant pressure of repayments can create a sense of financial vulnerability and stress. Even seemingly simple financial decisions become fraught with anxiety, as every purchase is weighed against the looming burden of debt.

This altered perception can manifest in several ways. Individuals might adopt more risk-averse behaviors, forgoing potentially lucrative opportunities to avoid further financial strain. Conversely, some might engage in impulsive spending, attempting to alleviate the emotional distress associated with debt, only to exacerbate their predicament. This cycle of anxiety and reactive spending can create a vicious loop, making it increasingly difficult to break free from the constraints of debt.

Furthermore, debt can impact our self-perception and confidence. The feeling of being overwhelmed by financial obligations can lead to feelings of failure and shame, further complicating the process of managing finances effectively. This underscores the importance of considering not only the financial aspects of debt but also the significant psychological impact it can have on individuals.

Short-Term Relief vs Long-Term Mindset

The decision to take out a personal loan often stems from a desire for immediate relief. Facing an unexpected expense, such as a medical bill or car repair, can trigger a strong emotional response, leading individuals to prioritize short-term problem-solving over long-term financial planning. This immediate gratification, while understandable, can have significant consequences.

Conversely, a long-term mindset considers the broader implications of borrowing. It involves carefully weighing the benefits of the loan against the future burden of repayment, including interest charges and potential impact on credit score. This approach emphasizes financial responsibility and sustainable spending habits, acknowledging that immediate solutions shouldn’t compromise future financial stability.

The conflict between these two mindsets is central to understanding the psychology of personal loans. Individuals who predominantly adopt a short-term perspective may find themselves trapped in a cycle of debt, repeatedly using loans to address immediate financial needs without addressing the underlying causes or developing a plan for long-term financial security. Financial literacy plays a crucial role in bridging this gap, empowering individuals to make informed decisions and adopt a more balanced approach.

A balanced approach involves acknowledging the need for short-term solutions while simultaneously implementing strategies for long-term financial health. This might involve creating a budget, exploring alternative solutions to borrowing, and developing a comprehensive repayment plan to minimize the long-term financial impact of the loan. Ultimately, the goal is to find a path that addresses immediate needs without compromising future financial well-being.

Responsible borrowing requires a careful consideration of both short-term needs and long-term consequences. It’s about understanding the emotional drivers behind the decision to borrow while maintaining a clear-eyed perspective on the financial implications. This balance is essential for making informed decisions and achieving long-term financial success.

Why Emotional Spending Leads to Loans

Emotional spending, driven by feelings rather than rational needs, is a significant contributor to personal loan acquisition. When faced with stress, sadness, boredom, or even excitement, individuals may engage in impulsive purchases to temporarily alleviate these emotions. This retail therapy, as it’s often called, can quickly lead to exceeding one’s budget and accumulating substantial debt.

The immediate gratification derived from purchasing desired items overrides the long-term consequences of increased financial burden. This is particularly true for larger purchases that require financing, ultimately leading to the necessity of a personal loan to cover the outstanding balance. The psychological need for instant relief often outweighs the rational consideration of interest rates, repayment schedules, and the potential strain on future finances.

Furthermore, the ease of access to credit through online lenders and credit cards exacerbates the problem. The readily available credit facilitates impulsive spending, as the immediate financial impact is masked by the delayed repayment schedule. This accessibility fosters a cycle of emotional spending followed by reliance on loans to manage the accumulating debt, creating a potentially unsustainable financial situation.

Understanding the psychological drivers behind emotional spending is crucial in preventing reliance on personal loans for non-essential purchases. Recognizing the temporary nature of emotional relief gained from material possessions and developing healthier coping mechanisms are key steps toward building sustainable financial habits and avoiding the pitfalls of debt.

How Loan Repayment Can Build Discipline

Successfully repaying a loan can be a powerful tool for building financial discipline. The process inherently demands planning, organization, and consistent effort. Meeting regular payment deadlines instills a sense of responsibility and accomplishment, reinforcing positive behavioral patterns.

The structured nature of loan repayment fosters self-control. Borrowers must actively manage their finances, budgeting carefully to allocate funds for repayments while still covering essential living expenses. This requires conscious decision-making and resistance to impulsive spending, strengthening self-discipline muscles in the process.

Furthermore, the potential consequences of default – such as damaged credit scores and financial penalties – serve as a strong motivator. The fear of negative repercussions encourages borrowers to prioritize loan repayments, reinforcing the importance of adhering to a financial plan and maintaining consistent behavior. This builds resilience against impulsive spending and strengthens one’s resolve to achieve long-term financial goals.

Beyond the purely financial aspects, the successful completion of loan repayment cultivates a sense of self-efficacy. Overcoming the challenges involved in managing debt and meeting repayment obligations demonstrates personal capability and strengthens belief in one’s ability to achieve difficult goals. This newfound confidence can positively impact other areas of life, fostering a greater sense of personal responsibility and control.

Breaking the Habit of Unnecessary Borrowing

Understanding the psychology behind borrowing is crucial to breaking the habit of unnecessary debt. Many people borrow money impulsively, driven by a desire for immediate gratification or a perceived need to keep up with social pressures. This often leads to a cycle of debt that can be difficult to escape. The key to breaking this cycle lies in shifting your mindset and developing healthier financial habits.

One effective strategy is to consciously delay gratification. Before making a purchase, take time to evaluate whether it’s truly necessary or simply a fleeting want. Consider the long-term financial implications and ask yourself if you can comfortably afford the item without resorting to borrowing. This practice helps to foster a sense of financial responsibility and strengthens self-control.

Another important step involves creating a realistic budget. A well-structured budget provides a clear overview of your income and expenses, allowing you to identify areas where you can cut back and save money. This helps to reduce the reliance on borrowing to cover unexpected expenses or impulsive purchases. By tracking your spending, you gain a better understanding of your financial habits and can identify triggers for unnecessary spending.

Building an emergency fund is also vital. Having a financial cushion to fall back on eliminates the need to borrow money in unforeseen circumstances, such as job loss or medical emergencies. This fund provides a sense of security and reduces the stress and temptation associated with resorting to debt in times of crisis. Aim to save enough to cover at least three to six months’ worth of living expenses.

Finally, seeking professional financial advice can provide valuable insights and guidance. A financial advisor can help you develop a personalized financial plan, identify areas for improvement, and create a strategy for managing debt effectively. Their expertise can empower you to make informed decisions and break free from the cycle of unnecessary borrowing.

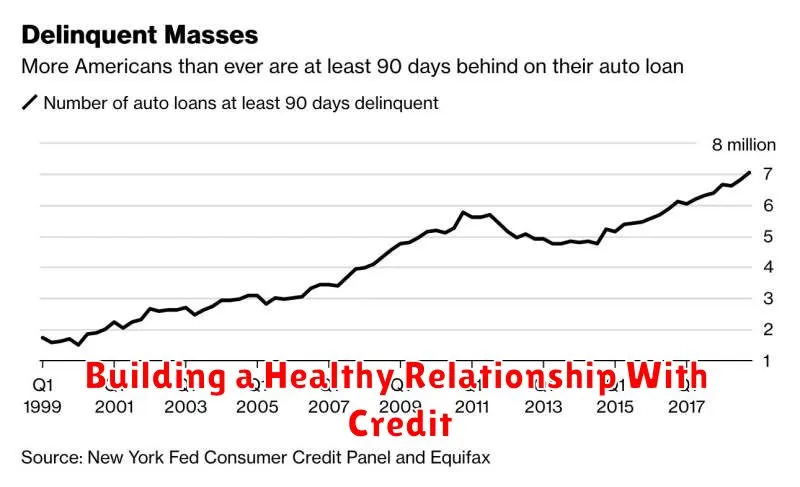

Building a Healthy Relationship With Credit

A healthy relationship with credit is crucial for long-term financial well-being. It’s not about avoiding debt altogether, but rather about understanding and managing it responsibly. This involves a conscious effort to build good credit and avoid the pitfalls of overspending and irresponsible borrowing.

The first step is to understand your credit score and what factors influence it. This includes your payment history, amounts owed, length of credit history, new credit, and the types of credit you use. Monitoring your credit report regularly and addressing any inaccuracies is vital.

Responsible borrowing is key. Before taking out any loan, thoroughly research the terms and conditions, including interest rates, fees, and repayment schedules. Only borrow what you can comfortably afford to repay, avoiding the temptation of accumulating excessive debt. Prioritize paying down high-interest debt first to minimize long-term costs.

Budgeting and financial planning are essential for maintaining a healthy relationship with credit. Create a realistic budget that tracks your income and expenses, allowing you to identify areas where you can save and allocate funds towards debt repayment. This proactive approach minimizes the risk of financial stress and promotes responsible credit management.

Seeking professional advice when needed is a sign of responsible financial management, not weakness. Financial advisors can provide guidance on debt management strategies, budgeting techniques, and long-term financial planning. They can help you develop a personalized plan to improve your credit health and achieve your financial goals.

Ultimately, building a healthy relationship with credit requires discipline, planning, and a proactive approach. By understanding your creditworthiness, borrowing responsibly, and managing your finances effectively, you can establish a solid financial foundation for the future. This positive relationship with credit empowers you to make informed decisions and achieve your financial aspirations.

{kind=link}