Are you looking for ways to harness the power of credit cards without succumbing to the pitfalls of debt? Mastering the art of responsible credit card usage can unlock significant financial benefits, from building credit scores to accessing convenient payment options. This comprehensive guide, “How to Use Credit Cards Wisely Without Falling Into Debt,” will equip you with the knowledge and strategies to navigate the world of credit responsibly. Learn how to avoid high-interest rates, manage your spending effectively, and ultimately achieve your financial goals.

This guide explores practical tips and proven techniques to help you avoid the common traps that lead many into credit card debt. We’ll delve into topics like choosing the right credit card for your needs, understanding credit card statements, and creating a budget to control your expenses. By the end of this article, you’ll have a clear understanding of how to use credit cards strategically to build positive credit history, secure rewards, and ultimately maintain financial stability without the burden of unmanageable debt.

Understanding Credit Card Limits and Utilization

Understanding your credit card limit and how to manage your credit utilization is crucial for responsible credit card use. Your credit limit is the maximum amount of credit your card issuer allows you to borrow. It’s a pre-approved amount, and exceeding it will likely result in penalties and declined transactions.

Credit utilization refers to the percentage of your available credit that you’re currently using. It’s calculated by dividing your current balance by your credit limit. For example, if you have a $10,000 limit and a $2,000 balance, your credit utilization is 20%. Credit utilization is a significant factor in your credit score.

Keeping your credit utilization low is essential for maintaining a good credit score. Financial experts generally recommend keeping your utilization below 30%, and ideally below 10%. A high utilization rate signals to lenders that you may be struggling to manage your debt, potentially leading to a lower credit score and making it harder to obtain future credit.

Monitoring your credit utilization requires regular checks of your credit card statements and online accounts. You should be aware of your spending habits and strive to pay down your balance before it reaches a high percentage of your limit. Making on-time payments is equally important, as late payments can negatively impact your credit score, regardless of your utilization rate.

By understanding and managing your credit card limit and utilization responsibly, you can significantly improve your financial health and build a strong credit history. This proactive approach helps avoid the pitfalls of debt and sets a foundation for sound financial management.

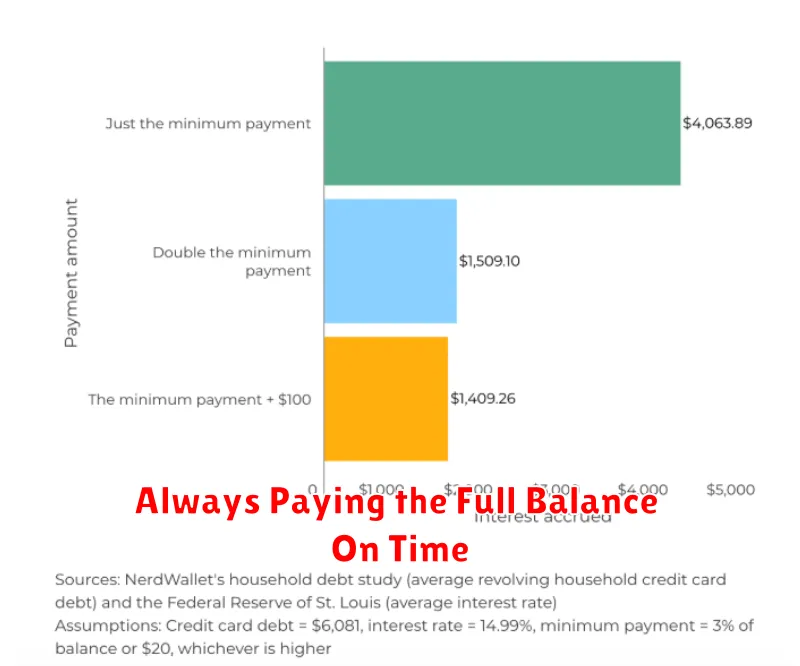

Always Paying the Full Balance On Time

One of the most crucial aspects of responsible credit card usage is consistently paying your full balance on time, every month. This seemingly simple practice significantly impacts your credit score and prevents the accumulation of interest charges.

Failing to pay your balance in full results in carrying a balance, which accrues interest at a potentially high annual percentage rate (APR). This interest can quickly spiral out of control, making it difficult to manage your debt and negatively impacting your financial health. By paying in full, you avoid these compounding interest payments altogether.

Paying your balance on time also demonstrates to credit bureaus your reliability and responsible financial behavior. This positive history contributes to a higher credit score, making it easier to secure loans, rent an apartment, or even obtain better interest rates on future financial products. The impact of consistent on-time payments is substantial and long-lasting.

While seemingly straightforward, maintaining this habit requires discipline and planning. Budgeting your expenses and tracking your spending can help ensure you have the funds available to pay your balance in full each month. Setting up automatic payments can also serve as a valuable safeguard against missed payments.

In short, always paying your credit card balance in full and on time is the cornerstone of responsible credit card management. It prevents the accumulation of debt, improves your credit score, and safeguards your financial well-being.

Tracking Your Spending Weekly

Effective financial management starts with understanding where your money goes. Tracking your spending weekly provides a clear picture of your spending habits and helps you identify areas where you can cut back.

There are several methods for tracking your spending. You can use a simple spreadsheet, a dedicated budgeting app, or even a notebook. The key is to choose a method that you find easy to use and maintain consistently.

When tracking your spending, be sure to categorize your expenses. Common categories include housing, food, transportation, entertainment, and debt payments. This detailed breakdown will reveal where the majority of your money is being spent.

Reviewing your weekly spending log allows you to make informed decisions. You can spot unnecessary expenses, areas where you can reduce spending, and identify potential problems before they become major financial issues. This proactive approach is crucial for maintaining a healthy financial life.

By diligently tracking your spending weekly, you gain valuable insight into your financial health. This empowers you to make responsible decisions and avoid accumulating unnecessary debt.

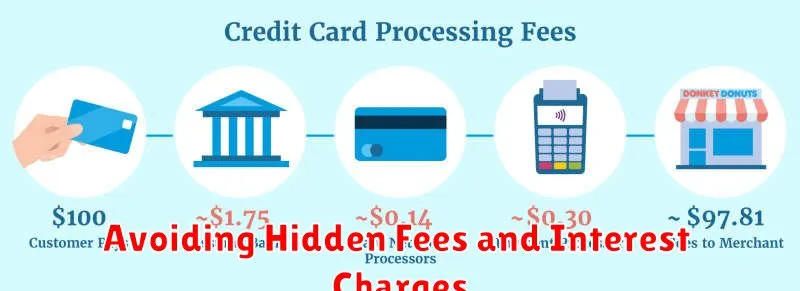

Avoiding Hidden Fees and Interest Charges

Understanding and avoiding hidden fees and interest charges is crucial for responsible credit card use. Many cards come with a variety of fees that can quickly add up, significantly impacting your finances. Careful scrutiny of the terms and conditions is paramount.

One common culprit is the annual fee. While some cards offer substantial rewards to justify this fee, others may not. Weigh the benefits against the cost carefully before applying. Consider whether the rewards program will genuinely offset the annual expense.

Late payment fees are another major source of unnecessary charges. Always prioritize paying your bill on time and in full. Setting up automatic payments can help avoid this pitfall. Even a single late payment can negatively affect your credit score.

Foreign transaction fees can significantly increase your expenses when traveling abroad. If you anticipate international travel, choose a card that waives or minimizes these fees. This is especially important for frequent international travelers.

Balance transfer fees, incurred when moving a balance from one card to another, can also eat into your savings. Understand the associated fees before transferring your balance. Carefully compare the interest rates of the new and old cards to ensure the transfer is financially advantageous.

Finally, understand the intricacies of interest charges. Paying only the minimum payment each month will result in accruing significant interest over time, leading to a snowball effect of debt. Aim to pay your balance in full each month to prevent the accumulation of interest.

By diligently reviewing your credit card agreement, understanding the fee structure, and consistently paying your balance on time, you can effectively avoid many hidden fees and interest charges, maximizing the benefits of your credit card while minimizing its financial risks.

How Credit Cards Affect Your Credit Score

Your credit score is a crucial three-digit number that significantly impacts your financial life. It determines your eligibility for loans, mortgages, and even insurance rates. Credit cards play a substantial role in shaping your credit score, both positively and negatively.

One of the key factors influencing your score is your credit utilization ratio. This is the percentage of your available credit that you’re currently using. Keeping this ratio low, ideally below 30%, is vital for a healthy credit score. Using a large portion of your available credit signals to lenders that you may be struggling financially, leading to a lower score.

Another important aspect is your payment history. Paying your credit card bills on time, every time, is paramount. Late payments severely damage your credit score. Even a single missed payment can have a noticeable negative impact. Consistent on-time payments demonstrate financial responsibility and contribute positively to your score.

The age of your credit accounts also matters. Having older accounts, especially credit cards, suggests a longer history of responsible credit management. This stability is viewed favorably by credit bureaus. However, opening too many new accounts in a short period can negatively affect your score.

Finally, the types of credit you utilize also influence your score. Having a mix of credit accounts, such as credit cards and installment loans, shows lenders that you can manage different types of credit effectively. This diversification can contribute to a better credit score.

In summary, responsible credit card usage is essential for building and maintaining a strong credit score. By understanding how these factors interact, you can effectively leverage your credit cards to improve your financial standing.

Best Practices for Building Credit With Cards

Building good credit is crucial for various financial endeavors, from securing loans to renting an apartment. Credit cards can be a powerful tool in this process, but only when used responsibly. Consistent and timely payments are the cornerstone of a healthy credit history.

One of the most effective strategies is to utilize a small percentage of your available credit. This metric, known as your credit utilization ratio, significantly impacts your credit score. Keeping your utilization below 30%, ideally closer to 10%, demonstrates responsible credit management. Avoid maxing out your credit cards at all costs.

Diversifying your credit is another important factor. While it’s beneficial to have several credit cards, focus on establishing a solid history with one or two before adding more. This shows lenders you can manage multiple accounts responsibly. Don’t open numerous cards in a short period, as this can negatively affect your score.

Regularly monitoring your credit report is essential. By reviewing your report from agencies like Equifax, Experian, and TransUnion, you can catch any errors or fraudulent activity. This proactive approach helps maintain the accuracy of your credit information and ensures your score accurately reflects your responsible credit behavior. Be aware of free credit reports you’re entitled to annually.

Finally, always pay your bills on time, every time. Even a single late payment can have a detrimental effect on your credit score. Set up automatic payments or reminders to avoid any potential missed deadlines. This consistent behavior is the most important aspect of building a strong credit profile with credit cards.

{kind=link}