Navigating the complex world of student loans can be daunting, especially for first-time borrowers. This beginner’s guide provides a comprehensive overview of the student loan process, from understanding different loan types and eligibility requirements to exploring repayment options and avoiding common pitfalls. Whether you’re a prospective college student, a parent helping your child finance their education, or simply seeking to better understand student loan debt, this guide offers essential information to help you make informed decisions and successfully manage your student loan journey.

Understanding the nuances of federal student loans versus private student loans, interest rates, and repayment plans is crucial for responsible borrowing. This guide will break down the complexities of student loan interest, loan forgiveness programs, and the potential long-term implications of student loan debt. We’ll equip you with the knowledge needed to minimize your debt burden and make student loan repayment as manageable as possible. Learn how to apply for financial aid, choose the right student loan for your needs, and plan for a financially successful future.

What Is a Student Loan and Why It Exists

A student loan is a type of loan specifically designed to help individuals finance their education. These loans are offered by various institutions, including the government and private lenders, and are intended to cover expenses such as tuition fees, accommodation, books, and other educational-related costs.

The existence of student loans is primarily driven by the increasing cost of higher education. Tuition fees at many colleges and universities have risen significantly over the years, often exceeding what many families can comfortably afford. Student loans provide a crucial financial mechanism enabling students from diverse socioeconomic backgrounds to access higher education, regardless of their immediate financial resources.

Furthermore, student loans are seen as an investment in human capital. A well-educated population is considered vital for a nation’s economic growth and competitiveness. By facilitating access to education, student loan programs contribute to the development of a skilled workforce, benefiting society as a whole.

While student loans offer a pathway to education, it’s important to understand that they represent a financial obligation. Borrowers are expected to repay the loan, usually with interest, after they complete their studies or after a specified grace period. Understanding the terms and conditions of the loan, including interest rates and repayment schedules, is crucial before taking out a student loan.

The availability of student loans also encourages individuals to pursue advanced degrees and specialized training, leading to enhanced career prospects and higher earning potential. This, in turn, helps contribute to both individual economic well-being and national economic productivity.

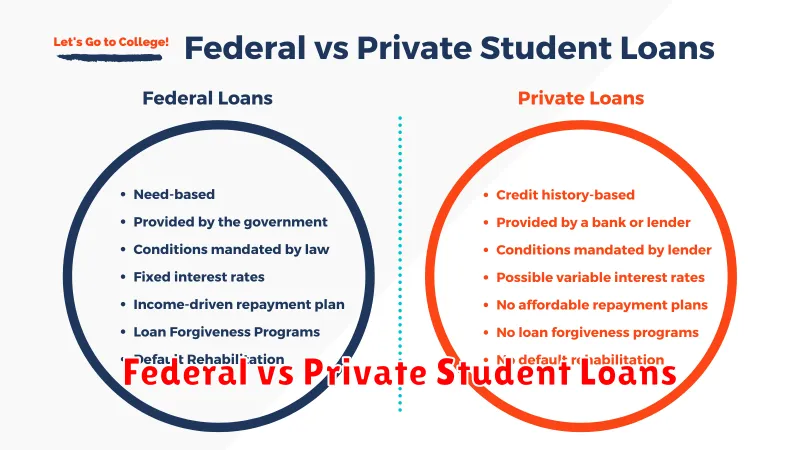

Federal vs Private Student Loans

Choosing between federal and private student loans is a crucial decision for prospective students and their families. Understanding the key differences is vital to making an informed choice that best aligns with your financial circumstances and long-term goals.

Federal student loans are offered by the U.S. government through programs like the Direct Loan program. A significant advantage of federal loans is the various consumer protections they offer, such as income-driven repayment plans, deferment options, and forbearance in times of financial hardship. These loans are typically less expensive than private loans, often with lower interest rates and fees.

Private student loans, on the other hand, are provided by banks, credit unions, and other private lenders. These loans are subject to the lender’s terms and conditions, which may vary widely. While private loans may be an option for those who have exhausted their federal loan limits, it’s important to note that they generally carry higher interest rates and may have more stringent qualification requirements. Borrowers should carefully compare loan offers from different lenders before making a decision.

A key distinction lies in the application process. Federal loans involve a straightforward application through the Free Application for Federal Student Aid (FAFSA). The application process for private loans varies depending on the lender, usually requiring a credit check and co-signer in many cases.

Ultimately, the best choice depends on individual financial situations and borrowing needs. Many students utilize a combination of federal and private loans to finance their education. It is highly recommended to fully explore federal loan options before considering private loans, given the greater protections and often lower costs associated with federal borrowing.

When Interest Starts Accruing

Understanding when interest begins accruing on your student loans is crucial for effective financial planning. The timing varies depending on the type of loan and your repayment plan.

For most federal student loans, interest typically begins accruing six months after you graduate, leave school (drop below half-time enrollment), or withdraw from your educational program. This grace period allows you time to find employment and prepare for repayment. However, there are exceptions. For example, some subsidized loans may not accrue interest during this grace period while unsubsidized loans will continue to accrue interest even during this period.

Private student loans often have different rules regarding when interest begins accruing. Some private lenders may start charging interest from the moment the loan is disbursed, even while you’re still in school. Others may offer a short grace period, but this is typically shorter than the grace period for federal loans. It’s essential to carefully review the terms and conditions of your specific private student loan to understand precisely when interest begins to accumulate.

The interest rate itself is another critical factor. A higher interest rate means that the amount of interest accruing on your loan will grow faster. Understanding your interest rate will allow you to better anticipate the total cost of your student loans.

Therefore, it’s vital to carefully examine your loan documents and contact your lender if you have any questions about when interest begins accruing and the specifics of your loan agreement. Being informed will help you to manage your student loan debt effectively and minimize the overall cost of borrowing.

Grace Period and Repayment Options

After graduating or leaving school, most federal student loan borrowers enter a grace period. This is a period of time, typically six months, before you are required to begin making loan repayments. During this grace period, interest may or may not accrue depending on the type of loan you have. It’s crucial to understand the specifics of your loan’s grace period to avoid accumulating unnecessary debt.

Once the grace period ends, you’ll need to choose a repayment plan. Several options exist, each with its own advantages and disadvantages, depending on your financial situation and loan amount. Standard repayment plans typically involve fixed monthly payments over a 10-year period. However, these payments can be quite high, especially for borrowers with significant loan debt.

Extended repayment plans stretch the repayment period to a longer timeframe, resulting in lower monthly payments but higher total interest paid over the life of the loan. Graduated repayment plans start with lower monthly payments that gradually increase over time. This can be helpful in the early years after graduation when income may be lower.

Income-driven repayment plans tie your monthly payments to your income and family size. These plans typically offer lower monthly payments, and any remaining balance may be forgiven after a set number of years, often 20 or 25, depending on the specific plan. However, it’s important to note that forgiven amounts are often considered taxable income.

Choosing the right repayment plan is a critical decision. Carefully consider your financial situation, long-term goals, and the implications of each plan before making your selection. You may want to consult with a financial advisor or your loan servicer to determine the best option for your individual circumstances.

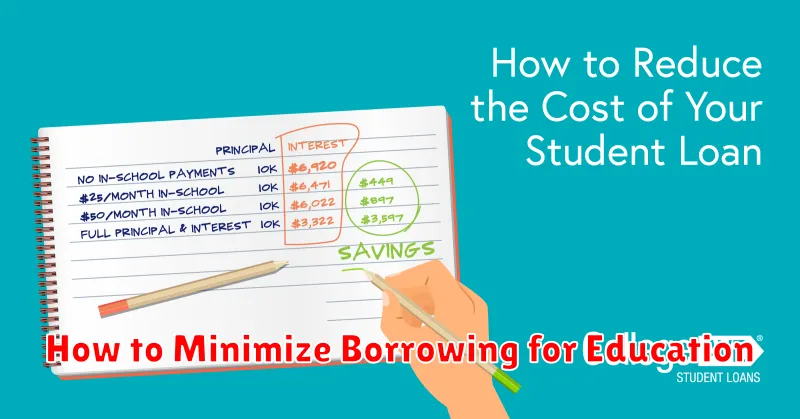

How to Minimize Borrowing for Education

Planning and preparation are key to reducing the amount you need to borrow for your education. Before even considering student loans, explore all available avenues to finance your studies.

Scholarships and grants are a fantastic starting point. These are forms of financial aid that don’t need to be repaid. Many scholarships are merit-based, rewarding academic achievement, while others are need-based, targeting students from low-income families. Thoroughly research and apply to as many scholarships as possible; even small awards add up significantly.

Savings and investments should be your first line of defense. If you or your family have accumulated any savings, prioritize using these funds towards education expenses before resorting to loans. Similarly, explore any existing investment accounts that could be tapped into responsibly.

Part-time employment can significantly reduce reliance on loans. Working during your studies, even for a few hours a week, can help cover expenses and lessen the financial burden. Choose employment that complements your academic schedule and doesn’t compromise your studies.

Careful consideration of educational expenses is crucial. Compare costs between different institutions and programs. Attending a less expensive college or community college for your first two years can drastically reduce overall borrowing. Think about the return on investment (ROI) of your chosen degree and whether it aligns with your career goals.

Exploring alternative educational paths should also be considered. Online courses, vocational training programs, and apprenticeships can offer more affordable paths to obtaining skills and knowledge. Weigh the pros and cons of these options to determine if they align with your career aspirations.

Finally, budgeting and financial planning are essential. Creating a realistic budget that accounts for tuition, fees, living expenses, and other costs will help you track your spending and make informed decisions about your finances. This will help you understand how much you truly need to borrow and make better financial choices throughout your education.

Understanding Loan Forgiveness Programs

Student loan forgiveness programs offer the potential to eliminate a portion or all of your student loan debt. These programs typically target specific professions, such as teaching, nursing, or public service, or are based on income levels.

It’s crucial to understand that eligibility requirements for these programs can be quite stringent. You often need to meet specific employment criteria for a set number of years, work for a qualifying employer, and maintain a certain income level. Furthermore, the amount of loan forgiveness available varies widely depending on the program.

Common types of loan forgiveness programs include Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and Income-Driven Repayment (IDR) plans that can lead to forgiveness after a certain period. Each program has its own set of rules and regulations, so careful research is essential.

Before relying on loan forgiveness, it’s important to consider the long-term implications. The application process for these programs can be complex and lengthy, and there’s no guarantee of approval. Moreover, some programs may require you to make payments for a significant period before becoming eligible for forgiveness. It is vital to carefully review the terms and conditions of each program.

It’s strongly recommended to consult with a financial advisor or student loan counselor to determine which forgiveness program, if any, is best suited to your individual circumstances. They can help you navigate the complexities of these programs and ensure you’re making informed decisions about your student loan debt.

{kind=link}